Real estate bonds and securitized real estate assets

Real estate bonds are fixed income capital market instruments secured by income producing assets (PMI). They come in the form of a real estate or mortgage surety.

Real estate bonds are generally high yielding medium term bonds issued by real estate developers and construction companies to finance real estate development projects during their construction phase. Mortgage bonds are long-term corporate bonds secured by the collateralization of specific commercial real estate held by the issuer, such as land and buildings.

A covered bond is a generally fixed rate capital market debt instrument secured by both the creditworthiness of the issuer and a pool of high quality collateral, primarily mortgages or high quality public sector loans. They are issued directly by a financial institution responsible for repayment of the security and backed by the special collateral pool.

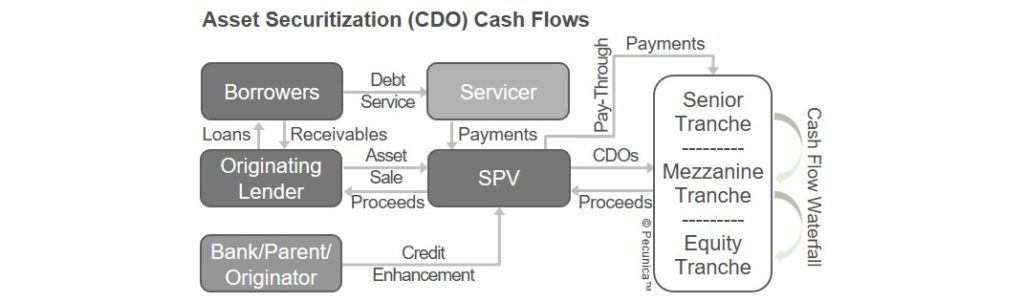

A Mortgage security (MBS) is a securitized debt instrument that represents a claim on the cash flows from mortgages pooled in a single pool that acts as collateral for the securities. Like a passage security, interest and principal payments received by the issuing SPV on the pooled assets are transferred to investors in equal measure during the same period received net of service charges, with each investor having equal rights to the flows cash.

Large commercial properties can be financed by commercial mortgage-backed securities (CMBS) as a collateral mortgage obligation (Marketing director). Like a payment security, the payments received by the SPV on the pooled loans are first used for the payment of the senior tranches, then paid to the more junior tranches only when the senior claims of the senior creditors are fully satisfied (the “cash cascade“).

The Commercial Mortgage Backed Securities (CMBS) market, a major source of capital for many hotel owners. Of the $ 300 billion in CMBS loans in the United States, hotels account for $ 86 billion in debt in 2019.

Syndicated loans and Club CRE

Syndicated loans is a multilateral loan initiated, organized and structured by one or more commercial or investment banks and marketed to a group (“syndicate”) of underwriters and / or lenders. Syndicated facilities are marketed to other banks and investment entities on behalf of the borrower in order to secure its commitment to provide the required financing.

A syndicated facility is financing in which a revolving credit facility and / or term loan is set up and provided through direct syndication and or funded participation by more than one lender under uniform terms and conditions using common documentation. Syndicated loans are administered by a common party – usually the originator of the loan and the principal arranger.

When the amount of financing required by a borrower is too large for a relationship bank to provide on its own, a club deal can be concluded. In a club agreement, a group of banks guarantees the full amount of a multilateral loan at the start of the transaction with no intention of subsequently reducing their investment in the loan (“final hold”). The club deal syndicate is closed when the facility agreements are executed (signed), without general syndication and without subsequent negotiation of the loan in the secondary market.

Syndicated real estate loans finance new real estate investments / acquisitions, refinancing of existing facilities, real estate development as well as unsecured real estate loans and refinancing in difficulty. Commercial and investment banks account for the majority of participation in syndicated real estate finance, followed by private equity and debt funds, insurers and pension funds, and construction companies.

Funds predominate in the leveraged loan, real estate and infrastructure debt markets. Hedge funds, CLOs / CDOs and distressed debt funds provide mezzanine and subordinated debt in real estate acquisition and development and investing frequently ready-to-own investments. Alternative credit investors, such as direct loan funds, provide debt in the middle market.

Private Debt Funds and Debt REITs

A private debt fund is a direct loan fund, usually in the form of a investment company with fixed capital, generally only for investment by institutional investors and high net worth individuals (HNWI). Individuals generally provide private debt through crowdlending platforms and by investing in debt mutual funds, which also lend to real estate companies.

Private debt funds are commonly used for direct loans for building construction and acquiring real estate. Real estate developers also often lend against the projects of other developers since they have experience in this type of financing.

Mortgages on properties serve as collateral for lenders in private debt funds, which allow the fund to take control of the underlying property in the event of default on their loans. Interest payments are the main source of return on their investments.

A confidence in real estate investment (REIT) is a corporation, trust or association that finances, generally owns and operates income-producing property or related assets for its investors. REITs issue transferable certificates that prove ownership, a creditor position, or both in the form of an equity REIT, debt REIT, or hybrid REIT, respectively.

Debt REIT lend money to real estate developers, sponsors and buyers in the form of debt or debt-like instruments, including first mortgages, mezzanine loans and preferred shares. Debt REITs generate income from interest earned on debt.

A Mortgage REIT highlights a creditor position in mortgages either made directly to buyers of real estate, developers and sponsors, or to invest in outstanding mortgages or mortgage backed securities (MBS). It generates income mainly from the net interest margin on investments – the difference between interest earned and the cost of financing loans.

For tax exemption, REITs are generally required to distribute at least 90% of their annual taxable income to their shareholders. This applies to US REITs and REITs in most European countries.

Copyright © 2020 Pecunica LLC. All rights reserved.